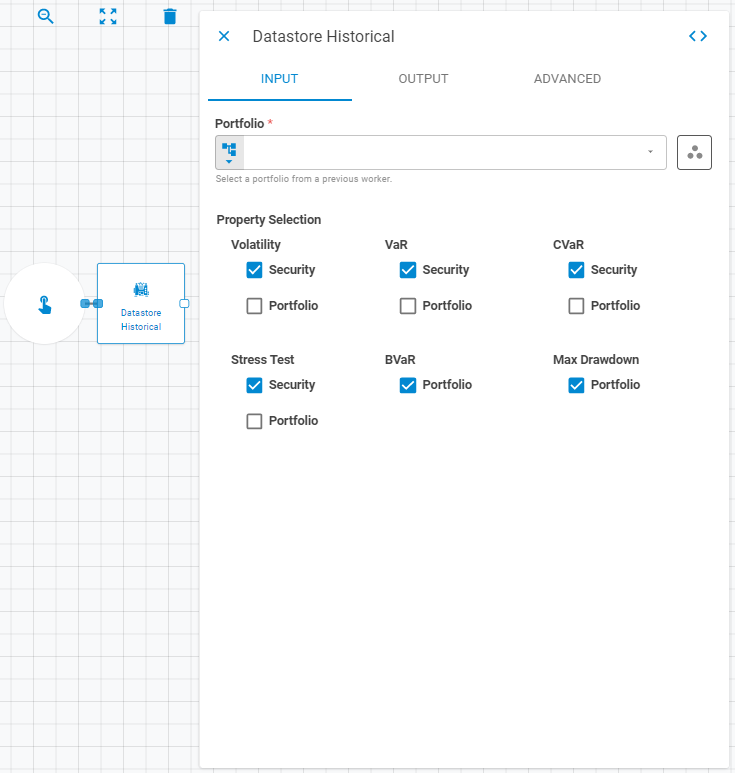

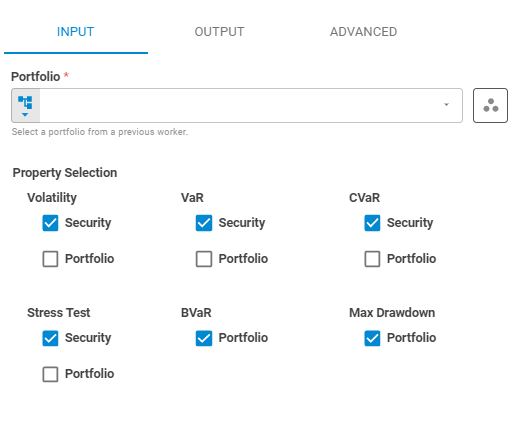

Datastore Historical¶

The Datastore Historical worker calculates the historical magnitude of a security's reaction to changes in underlying factors, and returns the results as a datastore.

Parameters¶

Input¶

| Field | Description |

|---|---|

| Portfolio | The target portfolio. Accepts Fixed Portfolio, Get Latest, or Upstream Data |

| Workspace | Workspace of the portfolio. Accepts Fixed Workspace. Defaults to the current workspace |

| Volatility | Whether to calculate volatility at the Security and/or Portfolio level. Accepts Boolean |

| VaR | Whether to calculate Value at Risk at the Security and/or Portfolio level. Accepts Boolean |

| CVaR | Whether to calculate Conditional VaR at the Security and/or Portfolio level. Accepts Boolean |

| Stress Test | Whether to calculate stress test results at the Security and/or Portfolio level. Accepts Boolean |

| BVaR | Whether to calculate Portfolio BVaR. Accepts Boolean |

| Max Drawdown | Whether to calculate Portfolio Max Drawdown. Accepts Boolean |

Output¶

| Field | Description |

|---|---|

| Name | Name of the output datastore. Accepts Template Text or Upstream Data. Defaults to the portfolio name |

| Date | Date of the output datastore. Accepts Fixed Date or Upstream Data. Defaults to the portfolio date |

| Workspace | Workspace where the output datastore will be saved. Accepts Fixed Workspace. Defaults to the portfolio workspace |

| Tags | Tags for the output datastore. Accepts Fixed Tags or Upstream Data. Defaults to the portfolio tags |

| Storage Mode | Transient — exists only within the current workflow run (default); Create — saves the datastore to the platform |

Advanced¶

| Field | Description |

|---|---|

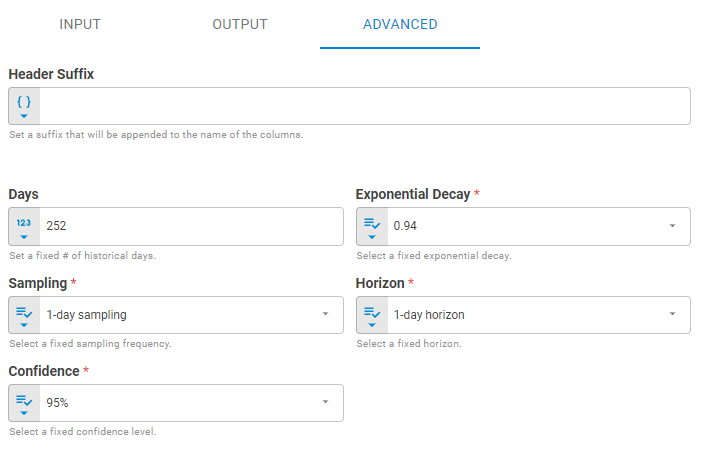

| Header Suffix | Suffix appended to the end of property column names in the output datastore. Accepts Template Text or Upstream Data. Default is no suffix |

| Days | Number of business days used to calculate the covariance for the primitive risk factors. Default is 252 |

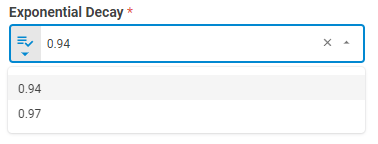

| Exponential Decay | Weighting factor determining the rate at which older data enters the calculation. Default is 0.94 |

| Sampling | Frequency at which historical prices and rates are sampled to compute risk factors. Use 1 for daily, 5 for weekly (non-overlapping). Default is 1 |

| Horizon | The forecast horizon for calculation. Produces a range of outcomes for each security via their underlying factors across a specific date range. Default is 1-day forecast |

| Confidence | Confidence level for calculation. For example, at 95% confidence with 10,000 simulations, the first 5% (500 samples) are used. Default is 95% |

Result¶

Once the worker finishes successfully, it returns a result object containing the datastore.

- Datastore (datastore)

- ID (string)

- Name (string)

- Date (date)

- Tags (list of strings)

- Data (list of lists)

The Data component includes the following columns:

port_historical_bvarport_historical_cvarport_historical_max_drawdownport_historical_st_dateport_historical_st_valueport_historical_varport_historical_volsec_historical_cvarsec_historical_st_valuesec_historical_varsec_historical_vol